Driving Consistent Growth Delivering Sustainable Value

A Proven Financial Track Record

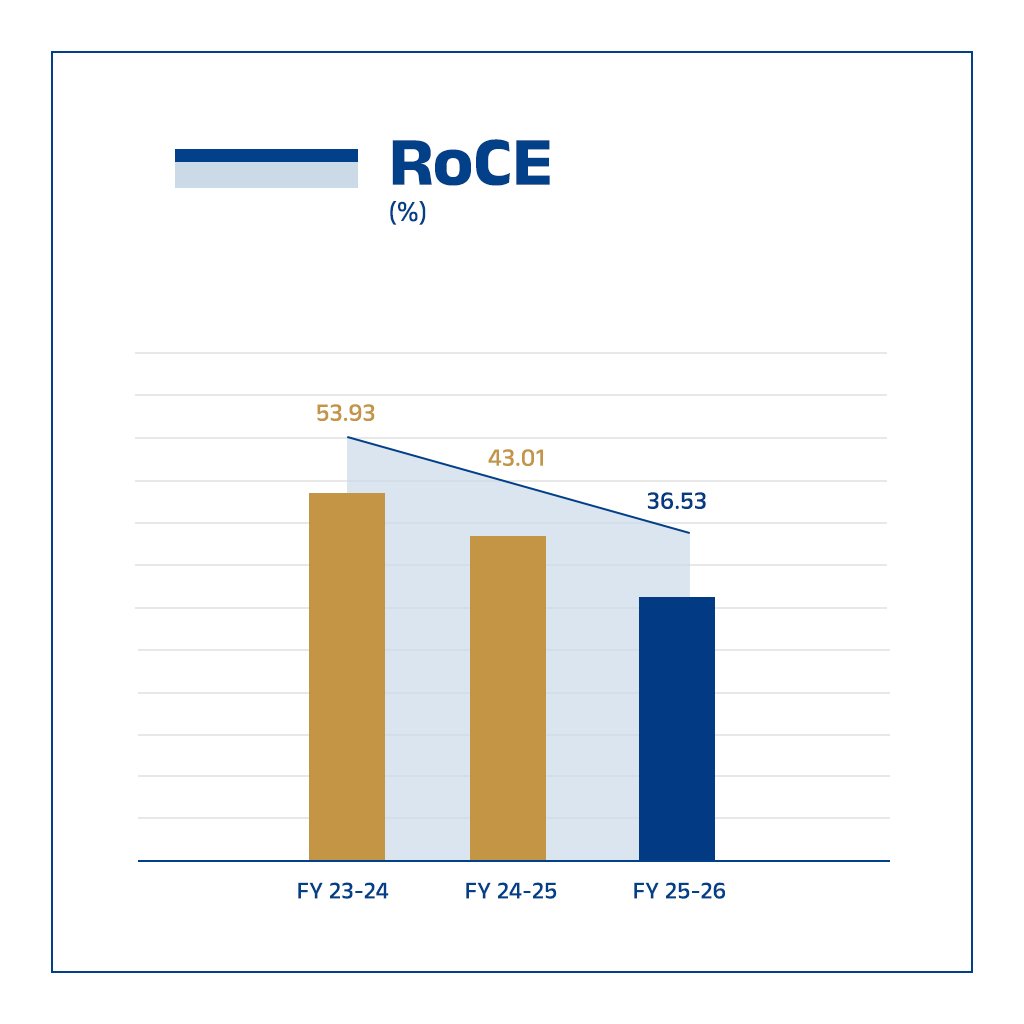

36.53%

Efficient capital deployment; superior returns.

#2 in India

Second-largest selling wood adhesive brand in the retail segment.

Net-Debt-Free

Robust balance sheet with zero net debt.

90% Dividend Declared

Consistent shareholder payouts.

Start a new journey!

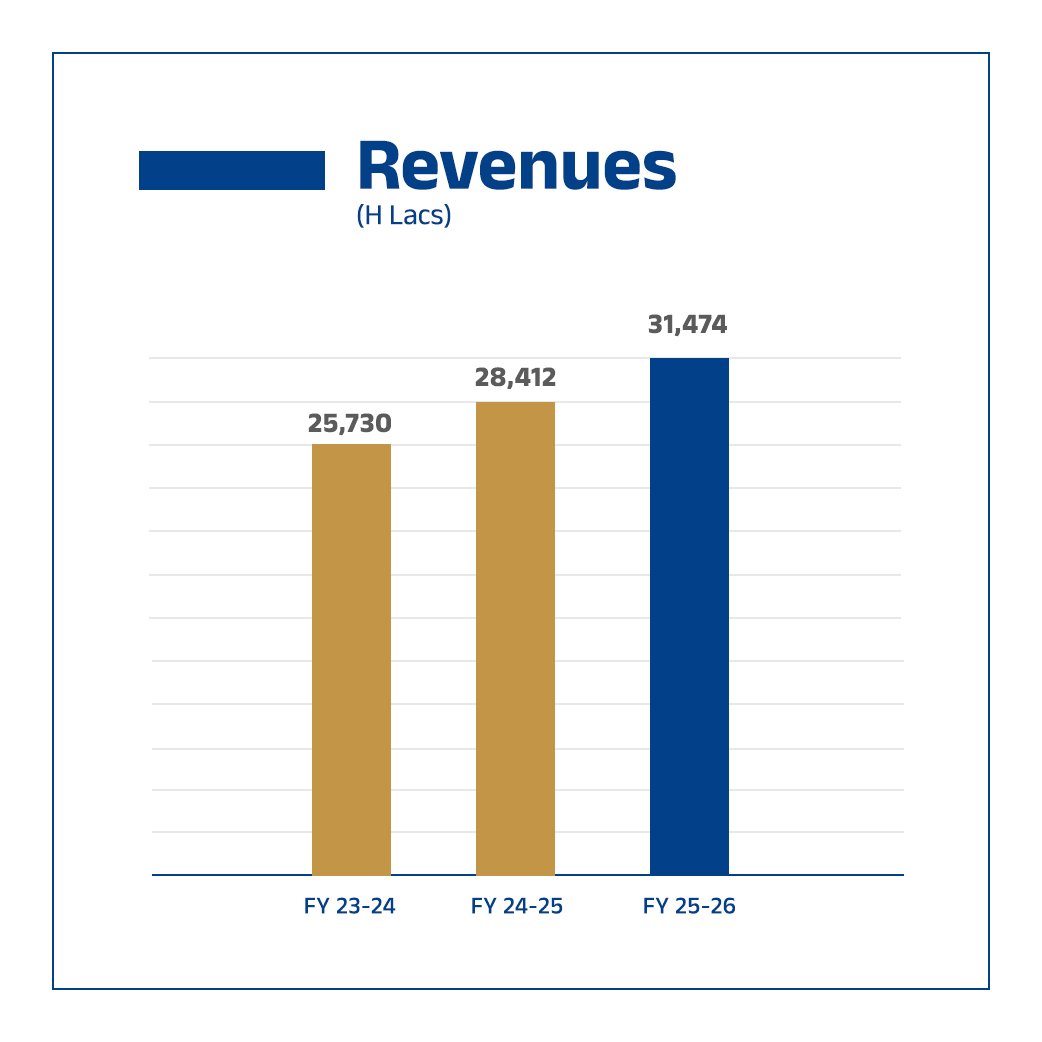

Revenues

Revenue scaled to ₹31,474 lakhs in FY 2025-26, registering 10.8% year-on-year growth on the back of deeper distribution reach, stronger pull for the Euro Adhesives brand, and continued penetration into newer geographies. The trajectory reflects the durability of consumer demand and the strength of our retail-led, carpenter-anchored go-to-market model.

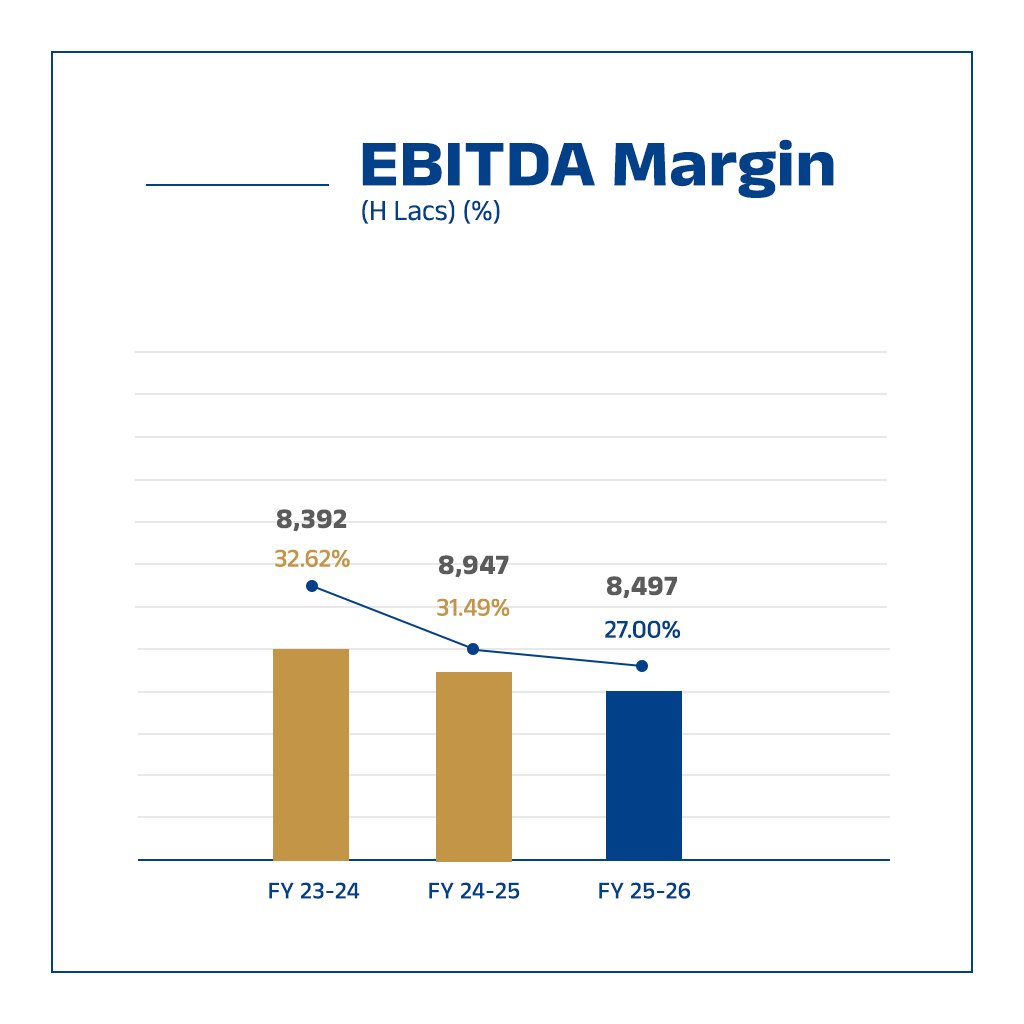

EBDITA MARGINS

EBITDA stood at ₹8,497 lakhs at a margin of 27.0% in FY 2025-26, with the moderation from the prior year reflecting a conscious step-up in brand-building, on-ground activations, and distribution investments aimed at consolidating market leadership. Margins remain structurally elevated and continue to compare favourably with industry peers.

Net Worth

Net Worth strengthened to ₹28,876 lakhs in FY 2025-26 — a 26% increase over the prior year and nearly 3x the level of FY 2022-23 — funded entirely through internal accruals. This sustained compounding of book value reinforces balance-sheet strength and provides ample headroom for future expansion without recourse to external capital.

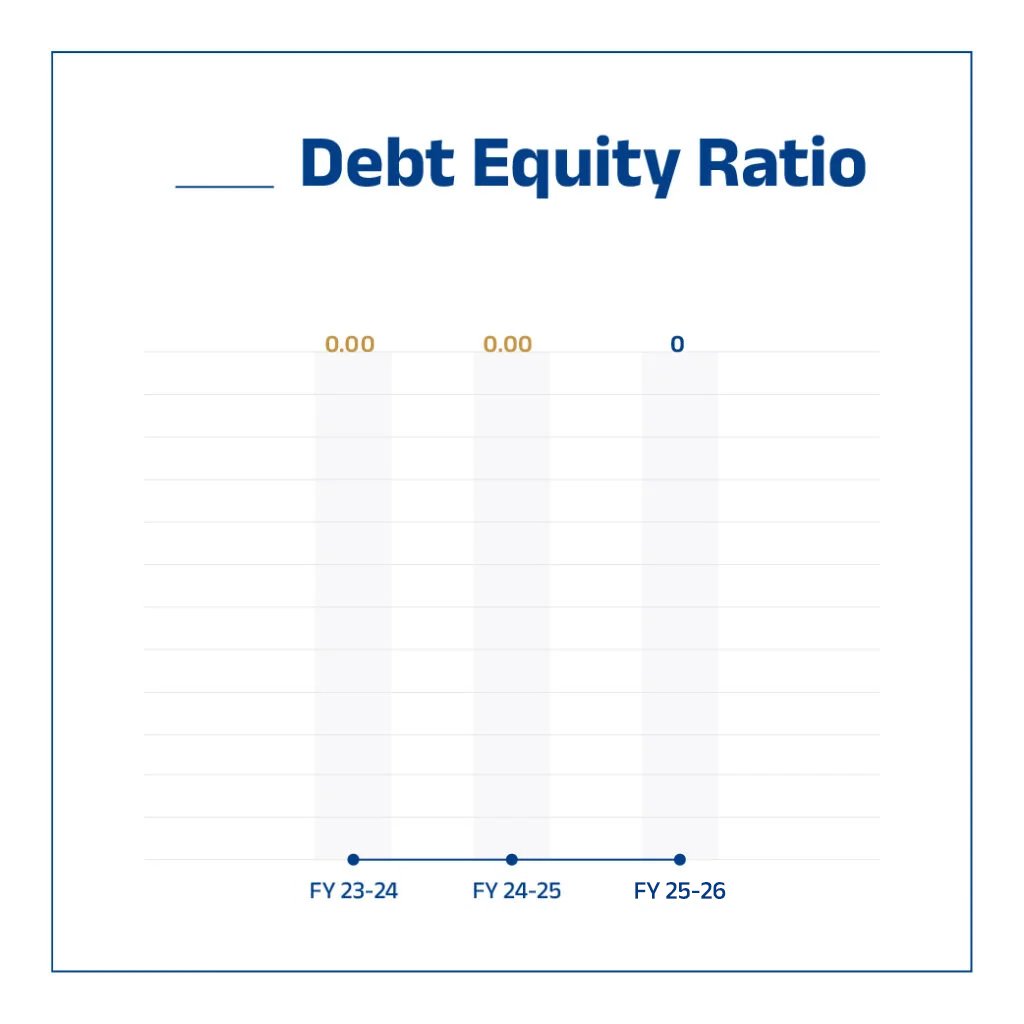

Debt-Equity Ratio

The Company remained debt-free in FY 2025-26, with a Debt-Equity ratio of 0.00 sustained through the year. This pristine balance sheet, funded by operating cash flows, provides resilience against macroeconomic volatility and the flexibility to pursue strategic opportunities on our own terms.

Return on Capital Employed (RoCE)

RoCE of 36.5% in FY 2025-26 reflects the capital-light, cash-generative character of our business and the discipline with which incremental investments are deployed. Returns continue to be delivered well in excess of the cost of capital — a hallmark of efficient, well-allocated growth.

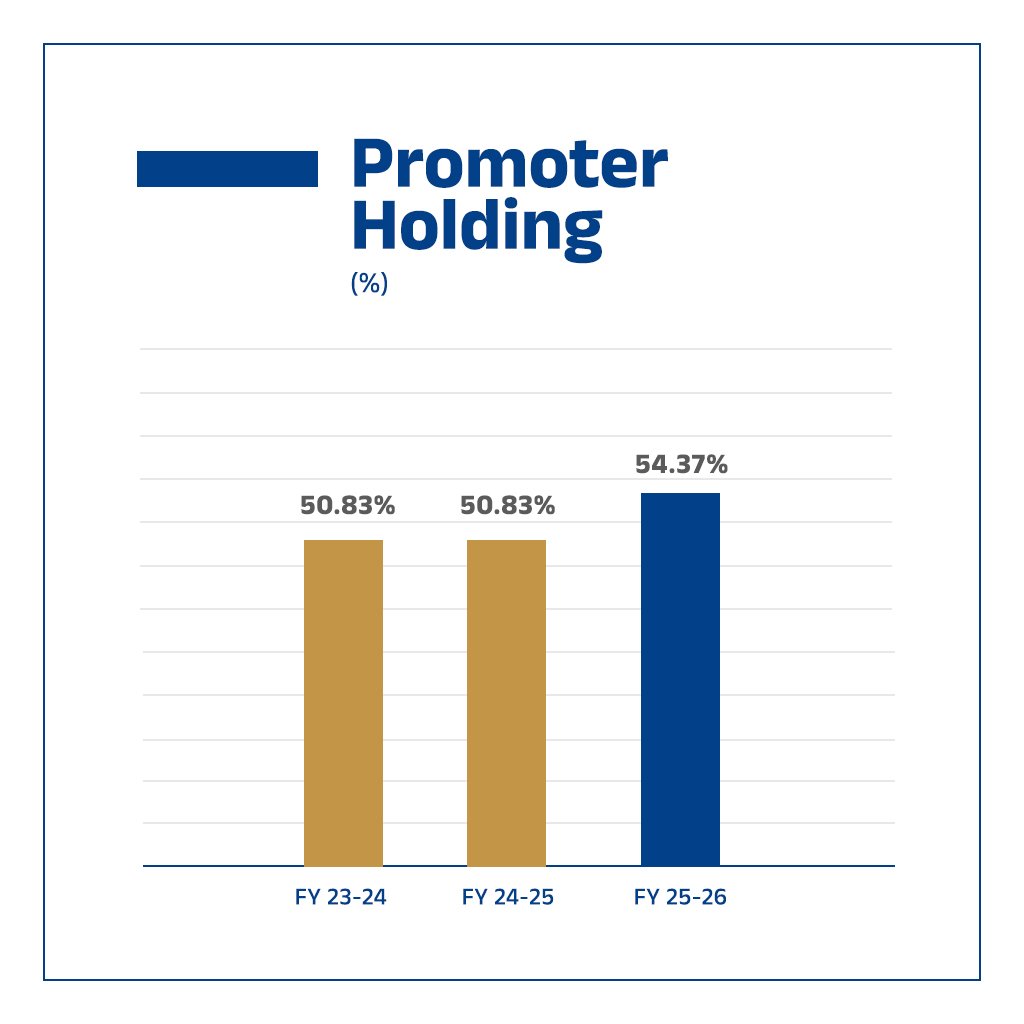

Promoter Holding

Promoter holding rose to 54.37% as on 31st March 2026, from 50.83% in FY 2024-25 — a meaningful increase that signals deep alignment with public shareholders and the promoter family’s strong conviction in the long-term value-creation journey of the Company.

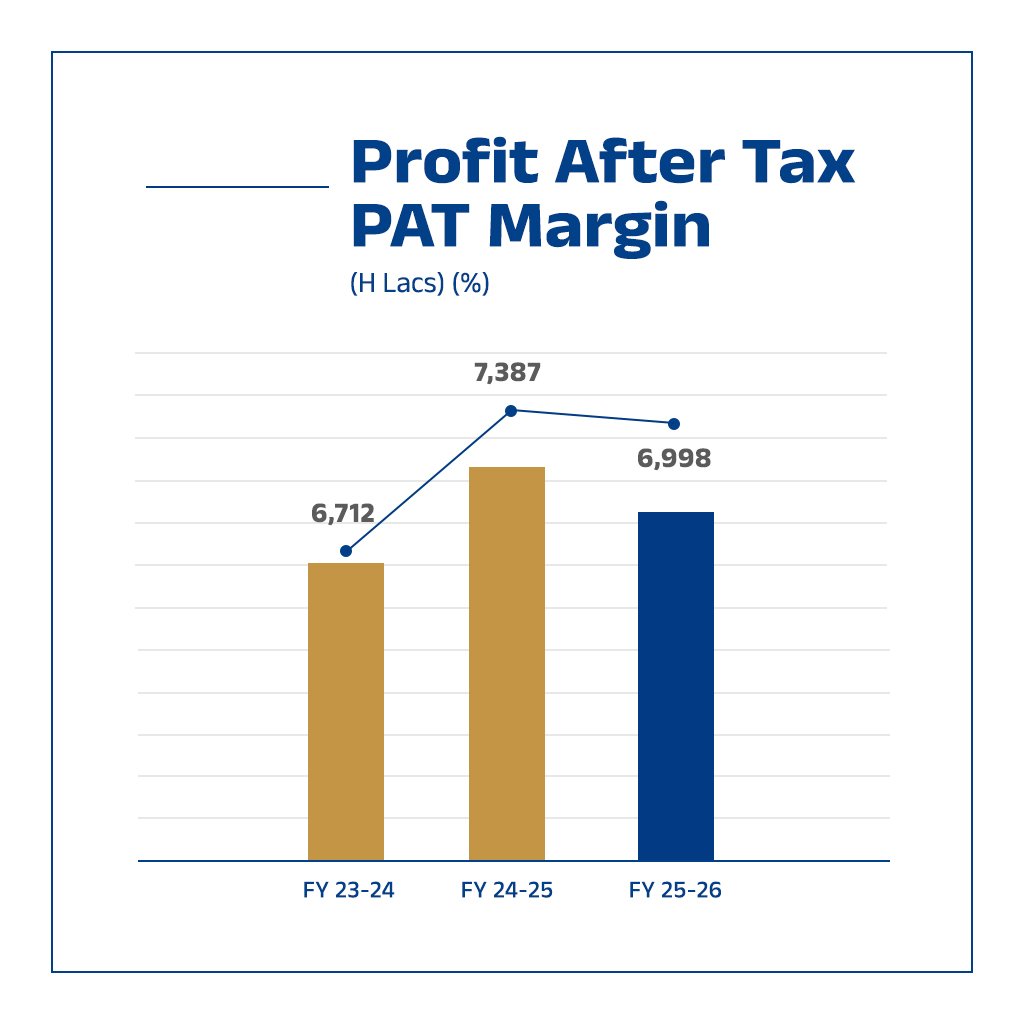

Profit After Tax (PAT) Margin

PAT stood at ₹6,998 lakhs in FY 2025-26 at a margin of 22.2%, with the year reflecting a calibrated trade-off between near-term profitability and forward-looking investments in brand and distribution. Absolute profitability remains robust — nearly 1.5x the level of FY 2022-23 — underscoring the resilience and quality of the underlying earnings engine.